If you are a freelancer in Pakistan, you already know the reality of the feast and famine cycle. One month, you close three massive international clients, and your bank account looks amazing. The next month, a client delays a payment, the dollar rate drops, and you get hit with a heart-stopping 60,000 PKR electricity bill.

I know this panic very well. In my journey running a digital agency, MZ Pro Services, and managing my job portal, I faced a major problem. I was making good money, but I had absolutely zero financial planning. I used to keep my hard-earned cash sitting idle in a standard Meezan Bank checking account, or worse, rotating it between SadaPay and JazzCash limits.

Money sitting idle in Pakistan loses value every single day because of inflation. I realized I needed a system. A system that protects my emergency cash, beats inflation, and grows my wealth over time.

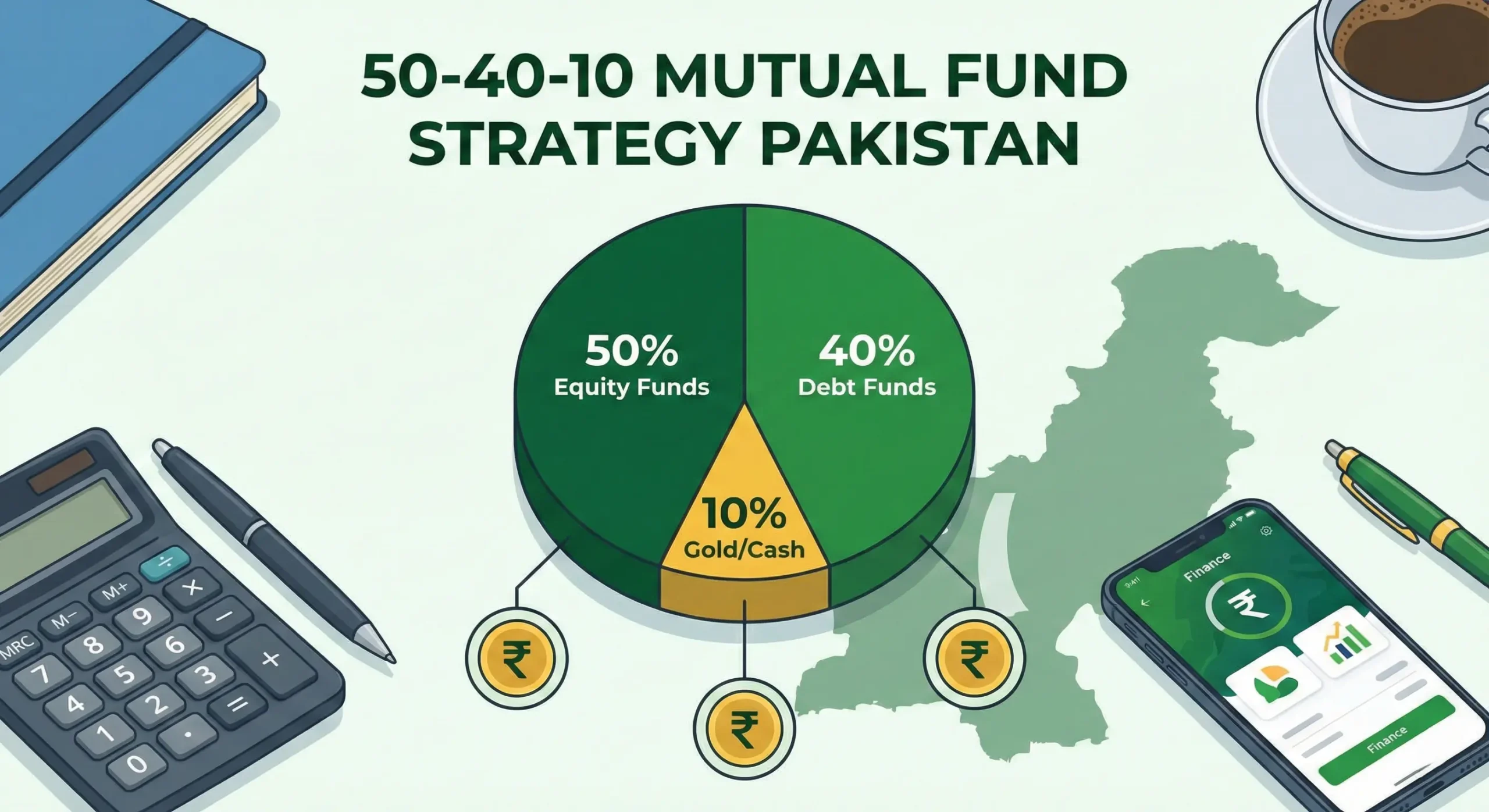

After experimenting with different investment vehicles, I developed what I call the 50-40-10 Mutual Fund Strategy. It is heavily tailored for the unpredictable nature of freelance income. Today, I am going to share exactly how I allocate my savings across different mutual funds to secure my financial future.

Table of Contents

Why Freelancers Cannot Invest Like Salaried Employees

Salaried employees get a fixed paycheck on the 1st of every month. They can afford to lock their money into a 3-year term deposit or buy long-term plots on installments.

As a freelancer, your income is highly irregular. You cannot lock all your money away because you might need immediate cash to upgrade a broken laptop, buy software subscriptions, or survive a dry month. We need high liquidity (the ability to withdraw cash instantly) without sacrificing profit.

That is the entire foundation of my 50-40-10 plan.

The 50%: Money Market Funds (The Safety Net)

Half of all my investment capital goes directly into Money Market Funds. This is your emergency fund. These funds invest in highly secure, short-term government and Islamic banking instruments.

My Choice: Meezan Rozana Amdani Fund (MRAF)

When I started taking investments seriously, I wanted to test the waters safely. I took PKR 83,000 and invested it into Meezan Bank’s MRAF. I was instantly hooked by the psychology of it.

Here is why I keep 50% of my portfolio here:

- Daily Profit: Unlike other funds that update monthly, MRAF adds a small profit to your account every single day. Seeing your balance increase daily keeps you motivated to save more.

- Zero Risk of Loss: Because it is a money market fund, your principal amount never goes down in negative figures.

- Instant Liquidity: If my car breaks down or a massive WAPDA bill arrives, I can redeem my MRAF units through the Meezan mobile app. The money hits my regular checking account within 24 hours. No penalties, no front-end load fees.

This 50% allocation ensures I always have cash on hand, but that cash is actually working for me instead of rusting in a current account.

The 40%: Islamic Income Funds (The Inflation Beater)

Money market funds are safe, but their profit rates often fall slightly behind real-world inflation. To counter this, the next 40% of my portfolio goes into Income Funds.

My Choice: Meezan Islamic Income Fund (MIIF) or MCB Alhamra

Income funds take a slightly different approach. They invest your money in medium-term Islamic bonds (Sukuks) and corporate papers. Because the money is invested for a slightly longer duration, the profit rates are generally better than MRAF.

- The Benefit: Over a 1-year period, income funds consistently provide solid, inflation-beating returns.

- The Trade-off: The unit price can fluctuate slightly from day to day. It is not a straight upward line like a money market fund. Additionally, withdrawing funds might take 2 to 3 working days instead of 24 hours.

I treat this 40% as my “1-to-3 Year Goals” fund. If I plan to upgrade my agency’s equipment next year, or save up to buy a new car, this is where that money sits and grows.

The 10%: Equity Funds (The Wealth Builder)

If you want to build actual, long-term wealth, you cannot ignore the Pakistan Stock Exchange (PSX). However, as a freelancer, I do not have the time to sit in front of a screen and analyze individual company stocks all day.

That is why the final 10% of my strategy goes into Equity Mutual Funds.

My Choice: Meezan Islamic Fund (MIF) or KSE Meezan Index Fund

An equity fund pools money from thousands of investors and buys shares in top-performing, Shariah-compliant companies (like fertilizer, oil, and IT sectors).

- The Reality of Equity: This is high-risk money. The PSX goes through wild swings. Some months your portfolio will be down by 10%. Other months, it will be up by 25%.

- The Mindset: I never put money here that I might need in the next five years. I treat this 10% as money that does not exist. Over a 5-to-10-year horizon, equity funds have historically delivered the highest compounding returns in the country.

(For current fund performance data, I always cross-check the official MUFAP Website before shifting my allocations.)

🚨 My Biggest Mistake

When I first started earning dollars, my financial discipline was terrible. My biggest mistake was waiting to “have enough money” before investing. I used to think mutual funds were only for rich businessmen sitting in corporate offices. I would leave my USD in my Payoneer account for months, hoping the dollar rate would go up, while ignoring the fact that I had zero PKR savings for local emergencies.

You do not need millions to start. You can open an Al Meezan investment account directly from their app with just PKR 5,000. Do not wait for a massive client payout. Start building the habit with whatever small amount you have right now.

💡 Personal Pro-Tip: The Auto-Debit Hack

As a freelancer, you have to be your own boss and your own HR department. You have to force yourself to save.

The best trick I learned is setting up an auto-debit instruction. I programmed my bank app to automatically deduct a specific amount from my checking account and push it into my MRAF mutual fund on the 5th of every month. I treat my investment account like my most aggressive client—I pay it first, no questions asked. If you do not automate it, you will end up spending that money on random Daraz sales.

How to Earn More So You Can Invest More

A strong investment strategy only works if you actually have money to invest. If you are struggling to find high-paying clients, you need to elevate your professional presence.

When I wanted to take MZ Pro Services to the next level, I stopped relying entirely on Fiverr and Upwork algorithms. I built my own independent portfolio website. Having a dedicated .com domain tells international clients that you are a serious agency, not a hobbyist. It allows you to charge premium rates, which in turn gives you more capital to dump into your mutual funds.

If you want to start building your own professional website, tech blog, or agency landing page, do not waste money on expensive setups. I personally use and highly recommend Hostinger Pakistan (Click Here for an Exclusive Discount).

Hostinger is extremely fast, highly secure, and most importantly, it fits perfectly into a beginner freelancer’s budget. You get a free domain and can launch your portfolio in under 20 minutes with their drag-and-drop builder. Secure your digital real estate today and start closing bigger deals!

Conclusion & Next Steps

Financial freedom as a freelancer in Pakistan is entirely possible, but it requires intentional planning. The 50-40-10 mutual fund strategy gives you the perfect balance of emergency liquidity, inflation protection, and long-term wealth generation.

Take a hard look at your bank account today. Calculate your monthly expenses, keep a small buffer in your checking account, and start pushing the rest into a money market fund immediately.

If you are looking to scale your income further, be sure to check out our detailed guide on How to Price Your Freelance Skills for International Clients right here on CareerTalks.

Stop letting your hard-earned money lose value. Be proactive, open your mutual fund account this week, and let your money start working for you!